Editorial Team

4 min read

- Mobile browser-based payments

- In-app mobile payments

- Mobile or wireless credit card readers

- Contactless mobile payments or mobile wallets

Mobile phones no longer function exclusively as communication devices. From alarm clocks to GPS tools to exercise apps, we’ve grown to rely on our smartphones for everything under the sun. We even use our mobile devices to make everyday purchases at retail shops, on eCommerce sites, and within apps.

Please share your contact information

to access our premium content.

Below are some of the most common ways in which we use our smartphones to send and receive mobile payments.

1. Mobile browser-based payments

Similar to desktop-based eCommerce shopping, mobile browser-based payments allow users to make card-not-present (CNP) purchases with either a credit, debit, or gift card, or even banking information (ACH) using a smartphone or tablet. Customers can visit a website with their mobile devices, add the products or services to a shopping cart, and enter payment details into the web site’s checkout form to complete a purchase – all on their phone or tablet.

2. In-app mobile payments

This type of payment is similar to a mobile browser-based payment; however, instead of navigating to a website, you can open up the app if that store or business has one. Users benefit from a range of in-app mobile stores and businesses that allow them to buy select products and services within closed ecosystems. Simply register your credit, debit, or ACH information once, and then you can purchase goods, download a book or song, buy a coffee, or pay a bill with a few clicks.

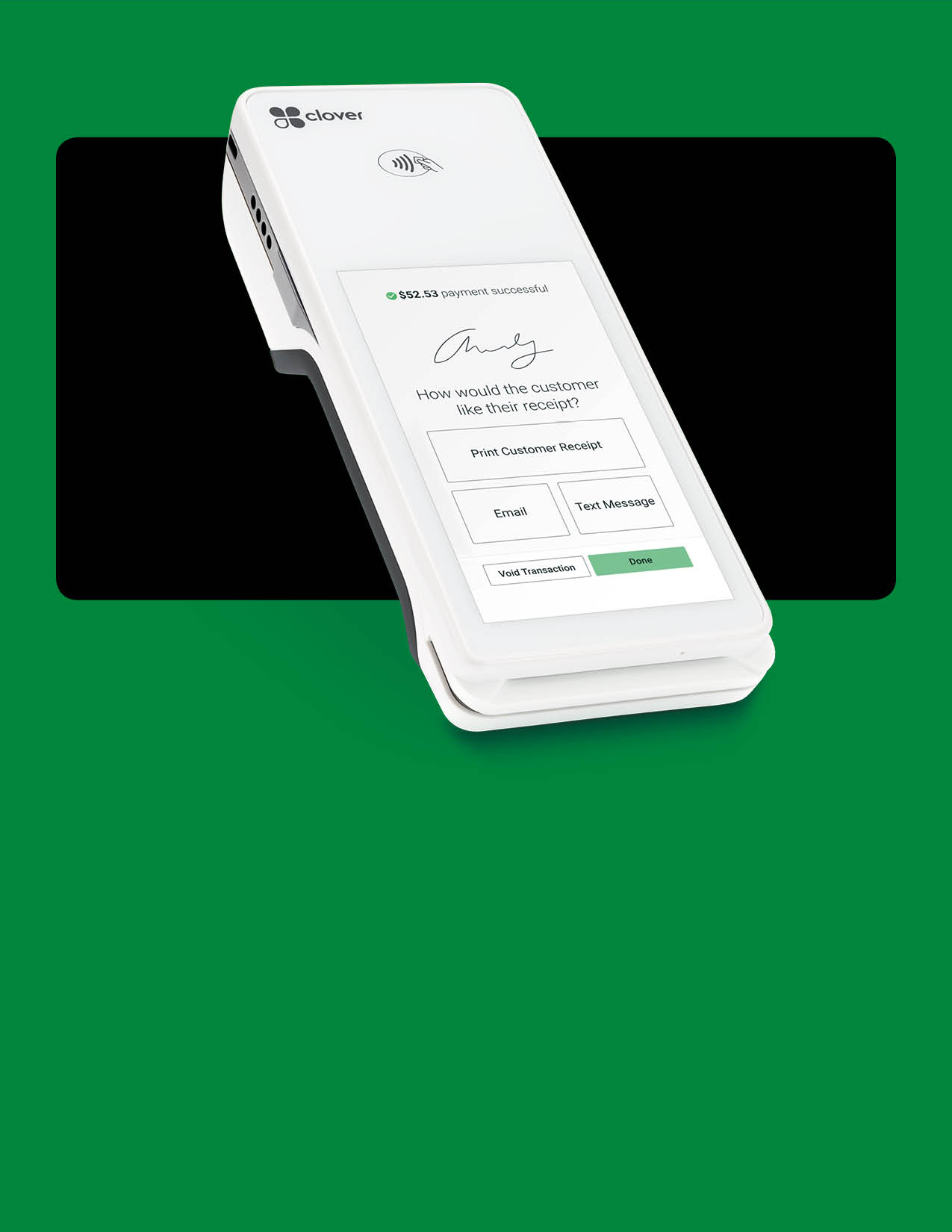

3. Mobile or wireless credit card readers

Rather than rely exclusively on stationary credit card terminals, businesses can turn smartphones or tablets into point-of-sale systems for on-the-go credit card acceptance by investing in add-on credit card readers that pair with the mobile device or fit into pre-existing headphone jacks. These mobile readers allow businesses to swipe, dip, or tap credit cards (just as they would with countertop terminals) and accept payments on the spot.

Other options to accept mobile payments is via a wireless credit card terminal or mobile credit card reader. This works and looks much like a traditional credit card terminal with a magnetic stripe or chip reader, keypad, and display screen. Wireless terminals do not require a direct hookup to a phone line, but instead, work off Wi-Fi to accept credit cards at various locations.

A credit card reader is not necessary for accepting mobile payments. Businesses can use a smartphone or tablet to log into a virtual terminal application and manually enter credit card or ACH information that way.

Any of these mobile payment solutions enable retailers to process transactions anywhere — including at off-site events like fundraisers, trade shows, and conferences. This technology also allows physical stores to harness the convenience of mobile payments.

4. Contactless mobile payments or mobile wallets

Bluetooth® and similar technologies have made it possible for shoppers and businesses to authorize transactions without having to physically swipe or dip any credit or debit cards at all. In order to complete a purchase, one simply has to wave his or her mobile device across a contactless reader that wirelessly (and securely) captures the relevant payment information.

Near field communication (NFC) is one of the technologies behind contactless payments. It’s similar to Bluetooth, but data transfers require closer proximity and offer greater security benefits. This technology is what powers payments behind mobile wallets like Apple Pay®, Samsung Pay, and Google Pay™.

Mobile wallets are not limited to in-store payments. Customers can checkout online using a mobile wallet wherever the preferred app is accepted.

Which mobile payment option is right for you?

Whether running an eCommerce store or a brick-and-mortar, mobile payments provide customers with convenient options that help deliver a seamless purchasing experience.

If you need help getting started with mobile payments, connect with a representative today.

Related Posts

Payment gateway vs. payment processor: what is the difference?

Accept credit card payments with an iPad POS system

Popular Topics

Stay in touch

Sign up and learn more about Clover.

More posts about starting a small business

eBook